By Rich Harvey, CEO & Founder, propertybuyer

Written by: Rich Harvey, CEO & Founder

propertybuyer.com.au

Click here to watch Rich's Video

Where will property prices be in the next 20 or 25 years? This month we take a glimpse into the future of property prices around Australia and ask the question what will drive property prices further and where will they end up? We will also examine current property trends and how you can take advantage of the amazing compounding growth factor that property offers compared to other asset classes.

PROPERTY PRICES IN 2043 – OCTOBER Market Update

Looking ahead 20 or 25 years can seem like a stretch too far for the imagination. But as you get older and look back, it's hard to believe how quickly that time has gone! While I'm sure many of us have regrets in life, one of the most common regrets that I hear is that “I wish I'd got into the property market sooner.”

The property market in Australia has shown remarkable resilience and growth over the past 25 years. There's been some major economic events and challenges including the COVID-19 pandemic in 2020, Global Financial Crisis in 2008, Sept 11 Terrorist attacks, 2002 stock market crash, SARS virus, Asian currency crisis and more.

Yet in spite of this Australian property prices have continued to climb and defy the various economic downturns that occur.

Looking back over 30 years ago at my first house I bought in the Hills area for $240,000 - that same house is now worth around $1.8 million. I remember at the time going to the bank and getting a loan and feeling nervous about the level of debt that I was getting into. I was feeling stressed and wondering how long it would take to pay all this incredibly high debt back. Fast forward 30 years and my wife and I have now built a sizeable property portfolio and are continuing to buy property each year.

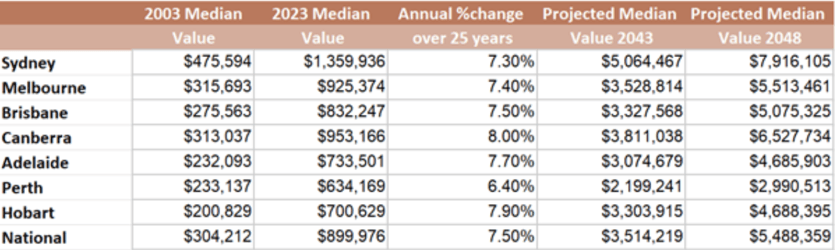

Twenty years ago, the typical median value of a house nationally was just $304,212.

Today in 2023, the national median house value sits around $900,000. This means that the typical Australian property owner who has held their house for the past 20 years has enjoyed a capital growth rate of around 7.5% per annum.

Where will prices be in 20 years’ time?

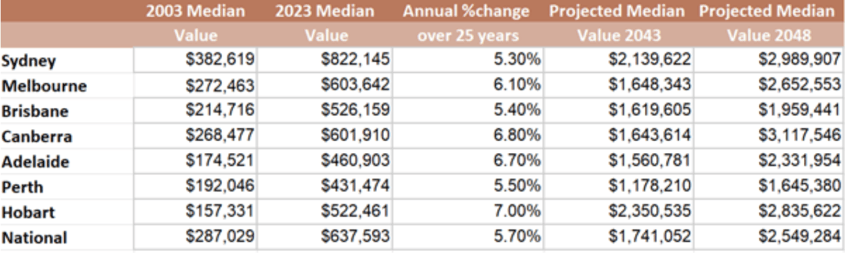

Taking the current median house prices in 2023 for each capital city and analysing the annual average growth over the past 20 years, I have then extrapolated the same average rate of growth to determine the projected median value in both 20- and 25-years’ time. See the results for both houses and apartments in the two tables below.

House Values in 20 & 25 Years

Apartment Values in 20 & 25 Years

If property prices continue to grow at the rate indicated above for each capital city, it will continue the trend of property prices doubling approximately every decade. It's interesting to note that growth rates tend to revert to the mean - and there is not a significant difference between each of the capital city growth rates over a longer period of time.

By the year 2043, Sydney is projected to have a median house value of over $5 million and Melbourne $3.5 million and Brisbane $3.3 million. And projecting further to the year 2048, Sydney is projected to have a median house value of over $7.9 million Melbourne $5.5 million and Brisbane $5 million.

When I showed these projected figures recently to a couple of groups, there was an immediate reaction, and I'm sure one of your reactions could be:

- Wow! How are my kids ever going to get into the property market?

- Oh gosh! There's no way I’ll be able to retire at 60 – I need to work for another 10 years.

- How will anyone be able to afford to buy a house without an inheritance?

- Prices are out of control.

- That's good news - I'm sitting pretty with lots of equity in my home. So pleased I bought 10 years ago.

- I really should consider recycling my equity into another investment property.

- Maybe its time to sell and downsize – great way to top up my SMSF.

What's driving property prices?

While these figures may appear large or unrelatable - you only need to think back to when the price of petrol was $0.30 a litre and a loaf of bread was $0.20. Price inflation creeps up on everything in the economy – even your tax returns and especially property. In fact, property is great hedge against inflation as it has always outperformed the inflation rate to provide a real return.

One of the fundamental factors driving property prices is the chronic undersupply situation in Australia. We are simply not building enough dwellings each year to satisfy ongoing demand. Building starts have averaged around 160,000 to 180,000 pa over the last 10 years. The federal government has recently announced ambitious plans to build over 1,000,000 properties in the next five years which will translate to 250,000 commencements per annum.

There are a significant number of logistical hurdles at the state planning level that must be overcome rapidly in order to achieve these kinds of targets and the states are also cracking down on building certifications to ensure dwellings are completed by reputable builders.

The migration wave into Australia, which is rapidly swelling our population numbers, is a major factor driving property prices higher. New migrants arriving in Australia tend to rent for two or three years before buying a property, so that is why the vacancy rates in all of our major cities is sitting at circa 1% vacancy or less in some cases. The high demand for rental properties is also pushing rents higher in every capital city and is likely to continue to do so for the next two to three years or more. Additionally, migrants have been shown that they tend to prioritise convenience - so they love to live near community shopping facilities education precincts and transport networks.

The work from home phenomenon driven by the COVID-19 pandemic saw many people flee the cities and work remotely. However there seems to be a stronger pull back to the cities now as many companies are demanding three or more days a week in the office to spur on face-to-face collaboration. (I recently heard the acronym “TWATs” as referring to people that commute to the office Tuesday – Wednesday and Thursday”) – that’s why the traffic is so much lighter on Mondays and Fridays.

Intergenerational wealth transfer and the Bank of Mum and Dad

When examining property price growth figures over a long period of time it becomes clear that those who are on a stronger wealth trajectory are those that own property compared to those that don't. One of the key trends to watch over the next two decades will be the number of baby boomers passing on their wealth via inheritances. Compared to the 80’s when Baby Boomers were first home borrowers using about 20% of their income on their properties, today mortgages can be expected to contribute up to 72% of all their available income to secure the same style of asset.

We're seeing quite a number of clients that are getting support from the Bank of Mum and Dad in order to help boost their buying capacity and fund the deposit and more to make them competitive in the housing market. One of the frequently quoted goals that I hear when completing a strategy session with clients is they want to provide a safe and secure environment to raise their own family and then leave a legacy and decent inheritance for their own children.

The problem of procrastination

“Procrastination is the thief of time” and it also robs you of ability to build real wealth through property ownership and investing. The longer you delay the purchasing decision and process, the longer it takes to catch up. There's no point waiting until you have completely paid off the mortgage and all the kids have left home to then start thinking about building a property portfolio.

Investing during your 30’s, 40s and 50s can set you up for a very healthy retirement - but it's never too late to start. It's just so much easier when you have some borrowing capacity and at least a decade ahead of you to see decent capital growth take place.

.svg)

.svg)

.svg)